Is the yield curve still useful for predicting recessions?

In 2022, the yield curve suggested an economic downturn was around the corner, but the U.S. economy has continued to grow anyway

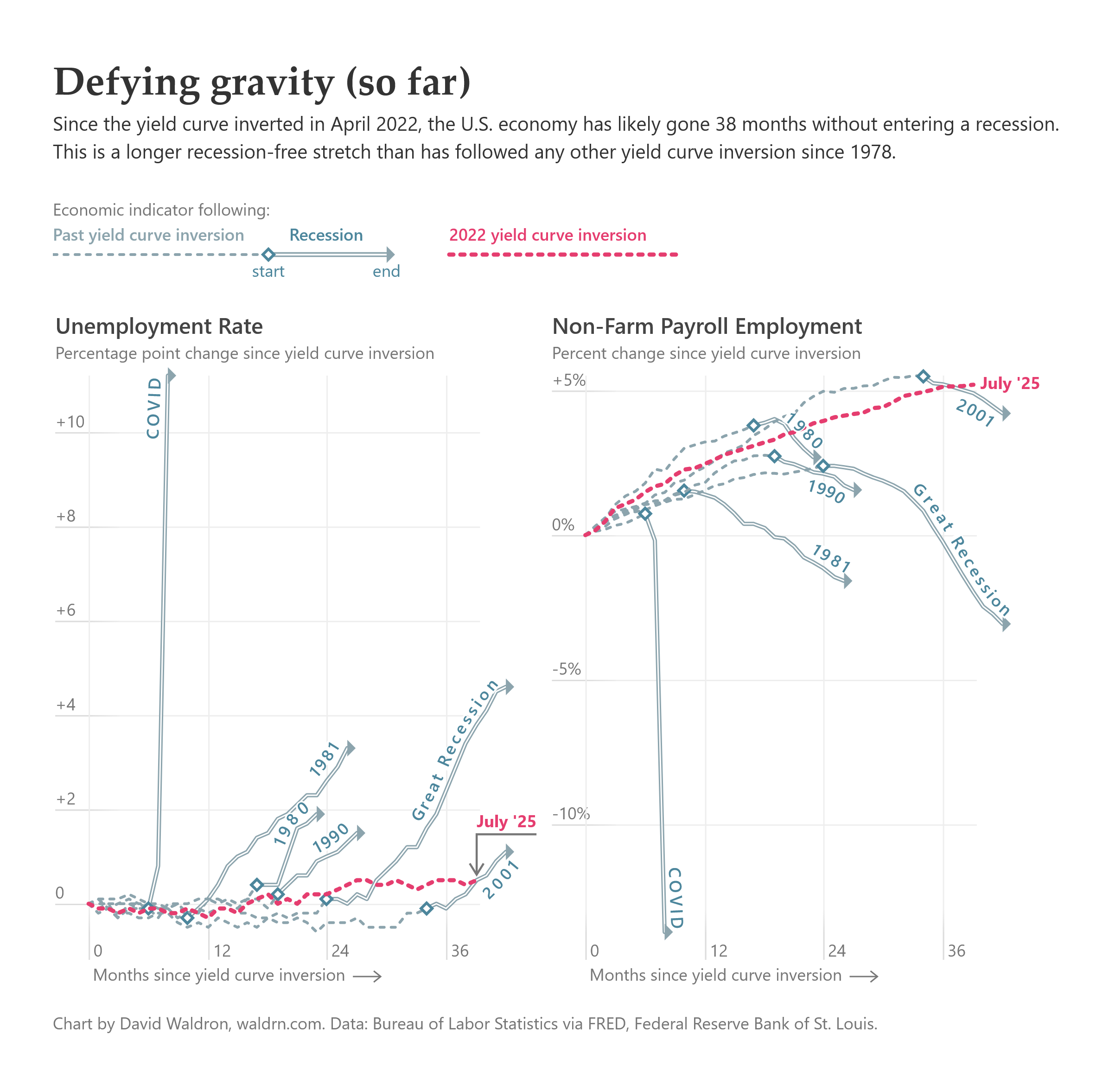

The yield curve, the difference between short- and long-term interest rates, has been a reliable indicator of future economic recessions for at least half a century. When the curve inverts, meaning short-term rates exceed long-term rates, this typically suggests that investors think the economy is nearing an economic downturn within the next year or two. But the last time the yield curve inverted was in April 2022, and as of July 2025, the U.S. economy has avoided recession for 38 months. This beats the 34 months between the 1998 yield curve inversion and the 2001 recession, making it the longest recession-free stretch following a yield curve inversion since 1978.

The yield curve wasn’t alone in predicting a recession. Following the yield curve inversion, a WSJ survey of economists rated a future recession as more likely than not for an entire year. A Bloomberg model declared a 100% chance of entering a recession before October 2023. The early warning Sahm indicator suggested that we’d entered a recession beginning in July 2024.

So far since 2022, unemployment has risen very slightly and leveled off around 4.2%. Payroll employment has increased consistently, continuing the second-longest streak of positive job growth since the series began in 1919. However, some cracks are beginning to show. July's jobs report suggests weaker growth in payrolls: The three-month average of net job growth has fallen to just 35,000.

Also troubling is that the integrity of future economic data is in jeopardy due to President Trump’s firing of BLS Commissioner Erika McEntarfer within hours of the report’s release. Trump accompanied the firing with groundless assertions that the numbers were “rigged” for political purposes. This politicization of economic data threatens the credibility of information that businesses, investors, and policymakers rely on for critical decisions.

Furthermore, Trump’s bizarre insistence on imposing constantly-changing tariff schedules on our trade partners and his continued obsession with deporting immigrants are likely to put downward pressure on the economy. Whether these policies are enough to push the economy into recession remains to be seen.